Congestion Pricing Delays Put $9B In 2024 MTA Capital Projects at Risk

ALBANY—New York State helped stabilize the MTA’s finances last year, but its capital program for maintaining and upgrading the regional transit system faces significant delays due to funding issues, which may also pressure its next capital plan, according to a report released on May 9 by New York State Comptroller Thomas P. DiNapoli.

“The MTA’s capital program is critical to winning riders back to public transportation and increasing fare revenue. When capital projects are delayed, repairs and upgrades are put off, causing parts of the system to deteriorate further,” Mr. DiNapoli said. “There’s more at stake than just delayed projects. If the MTA covers the shortfall in capital funds by using its operating budget to pay for more borrowing, less money would be available for day-to-day operations and goals, like increasing service.”

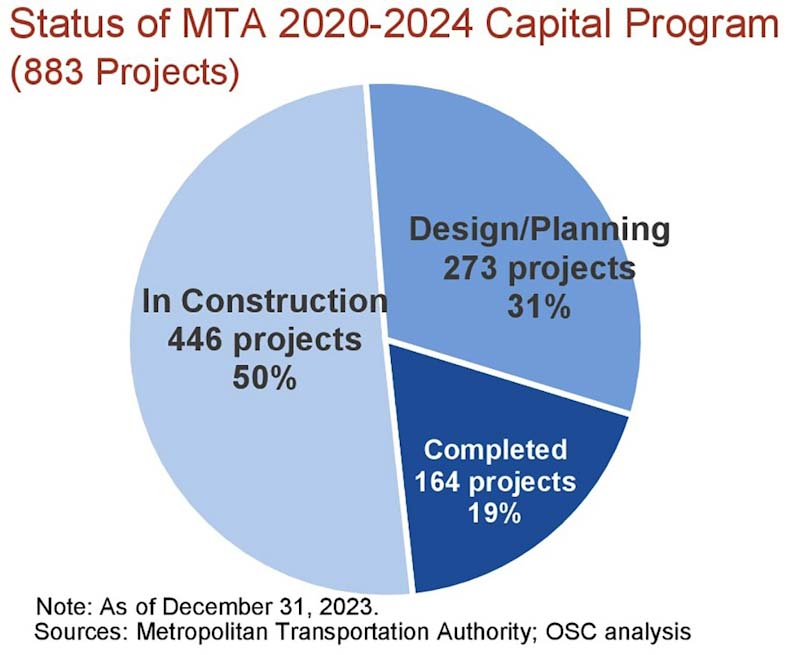

Capital Program Progress

As outlined in prior reports by Mr. DiNapoli, numerous parts of the MTA’s system are in poor condition, and the MTA relies on debt to pay for the capital improvement projects to maintain and repair the system.

Delays, uncertainties, and lawsuits around congestion pricing’s implementation have slowed down the MTA’s capital work. Before the pandemic, the MTA averaged $7.1 billion in commitments to capital projects (2016-2019). In 2022, it put a record $11.4 billion toward capital work. However, those commitments slipped to $8 billion last year and the MTA’s target for 2024, once estimated at $12 billion, is now less than $3 billion.

Congestion pricing was projected to provide about $15 billion of the MTA’s current $54.8 billion 2020-2024 capital program. Implementation delays have pushed back much-needed projects, with $9 billion in 2024 work currently at risk.

Given the MTA’s repair needs, its plans for resilience efforts, and its expansion projects, it is likely that the program will be at least the size of the previous program.

If other dedicated capital revenue sources are not available, there could be at least a $25-billion funding gap in the next capital program, which would create pressure to increase debt and impact the operating budget. Without additional money from better-than-anticipated tax and fare revenues or added savings from cost efficiencies, the MTA would eventually have to raise fares or tolls or cut service to cover such a gap, which would negatively affect riders’ experience.

Debt and Borrowing

Long-term debt outstanding issued by the MTA and supported by its operating budget more than doubled from 2000 to 2010, from $11.4 billion in 2000 to $29 billion in 2010, as the MTA funded a significant portion of its capital programs with bonds. The pace of growth slowed to 22% from 2010 to 2019, to reach $35.4 billion, as state and federal support rose from the decade prior. Since 2019, however, debt has risen to accommodate increased capital spending, reaching $40.4 billion in long-term debt paid from the operating budget in 2023, a 14% increase, the State Comptroller reported.

The MTA’s total outstanding debt is expected to rise from $42.4 billion in 2023 to $59.9 billion in 2028. A small but growing portion of this is funded outside of the operating budget (known as capital lockbox debt and funded primarily by future congestion pricing revenues), which is projected to make up 5% of debt in 2023 and 32% in 2028.

Debt service, which is the amount the MTA spends to pay down debt each year (including for lockbox debt), is projected to reach $5 billion by 2031, an 83% increase over 2023’s $2.3 billion. Historically, about 16% of MTA’s annual revenue is spent on debt.